Gold Gap Snapshot — June 2026

The gap narrowed this month. That's not the good news it sounds like.

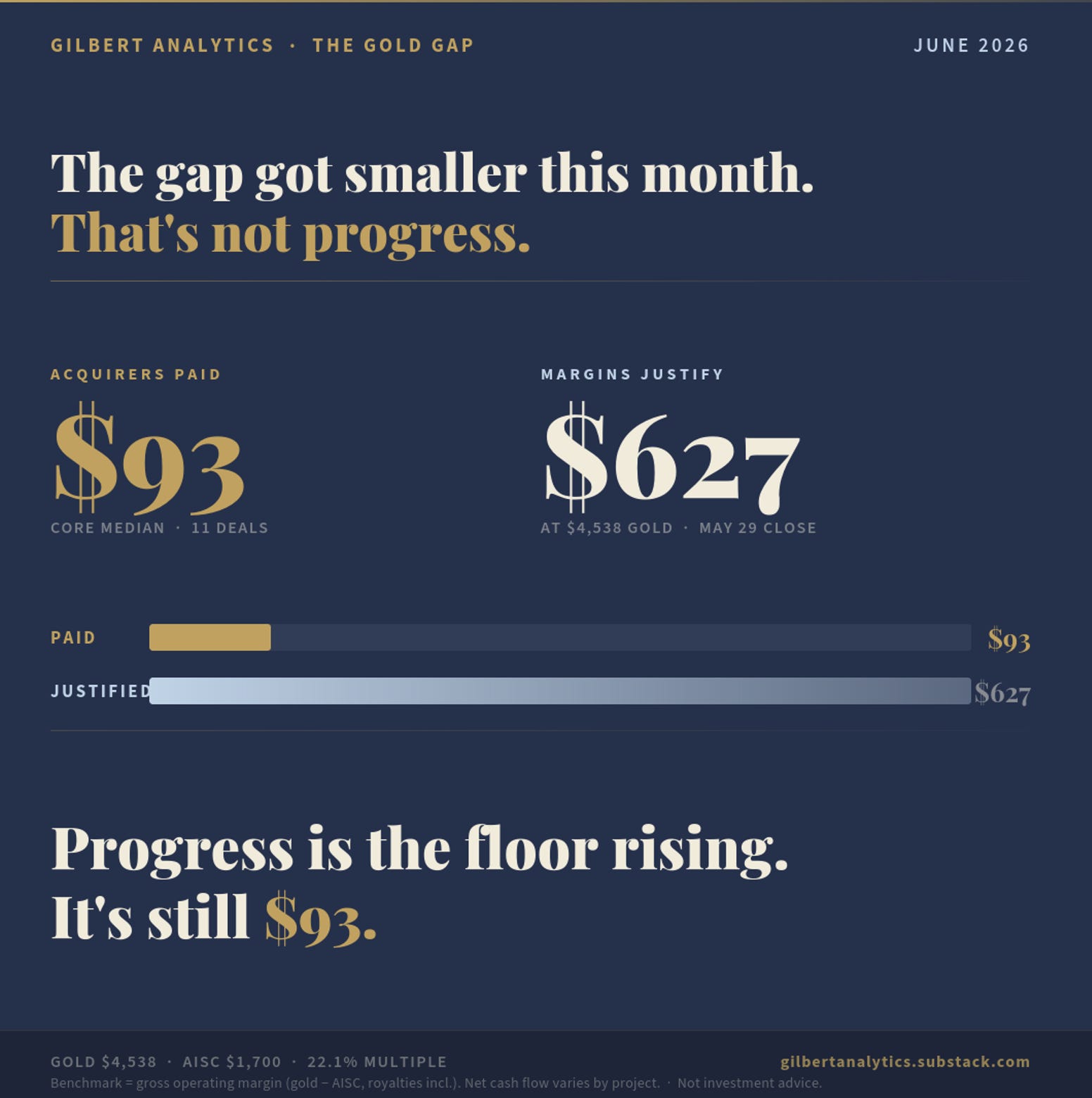

Last month, this snapshot put the gap at $551/oz USD. This month it’s $534. Smaller.

Read quickly, that looks like the disconnect starting to resolve. It isn’t — and the reason is worth thirty seconds.

The benchmark — what gold’s operating margins justify paying — fell from $644 to $627. That’s by design. Gold eased from about $4,614 to $4,538 at Friday’s close, the gross operating margin compressed with it, and the benchmark is a fixed share of that margin. Lower gold, lower benchmark.

The floor — what acquirers actually paid — didn’t move. $93/oz, the median across eleven transactions and five years of M&A data.

So every dollar of the narrowing came from the benchmark side. None came from acquirers paying more. The gap got smaller the way a shadow gets shorter toward noon: nothing about the object changed.

This is the distinction the Gold Gap is built to expose. A gap that narrows because gold fell is mechanical. A gap that narrows because acquirers bid up ounces in the ground is structural — a genuine re-rating. Only the second one means anything to someone holding a junior. And it hasn’t happened: the floor is still $93, the compression still about 85%.

Pull back and the point sharpens. Gold is down more than $1,000 from its January 29 high near $5,600 — roughly 19%. Up to that peak and all the way back down, acquirers paid $93. The floor doesn’t track the metal in either direction.

What actually closes the gap is the floor rising — acquirers forced to re-rate what an ounce in the ground is worth. The pressure for that builds on the demand side: producers are earning record gross margins while depleting reserves faster than they replace them through discovery. That’s the demand behind the Gap, and it doesn’t negotiate with spot. (For the full mechanism, see The Cycle Has a Sequence.)

So the next time the gap ticks smaller, ask which number moved. This month, it was the wrong one.

See the full interactive chart: gilbertanalytics.github.io/gold-gap/

If the gap can narrow without a single acquirer paying more, what would it actually take to make the floor move — and would you recognize it when it starts?

Benchmark uses gross operating margin (gold price minus AISC). AISC is the World Gold Council standard and includes mine-site royalties and taxes per ounce sold. Net cash flow to equity varies by project structure — IBA / First Nations participation, sustaining capex, and corporate taxes are project-specific.

Gilbert Analytics produces independent analysis of the junior gold mining sector. The Gold Grid is a systematic scoring and research publication. For methodology details, see GG-002, “What Acquirers Actually Pay for Gold in the Ground.”

The Gold Gap Index is a macro indicator based on publicly available M&A transaction data. It does not constitute investment advice. New to the Gold Gap? Start with GG-001: Mind the Gold Gap. See gilbertanalytics.github.io/gold-gap for the interactive chart.

Disclosure

The author, Alain Gilbert, holds positions in publicly traded junior gold companies. The author may also hold positions in other publicly traded companies discussed in this publication. All material positions are disclosed when relevant. This analysis does not constitute individual investment advice and is not designed to meet your personal financial situation or needs. The author is not a licensed financial analyst, registered broker-dealer, or investment adviser, and is not registered with the U.S. Securities and Exchange Commission, any state securities regulatory authority, or any self-regulatory organization. Never make an investment based solely on what you read in an online newsletter.

Results Not Typical. Any historical performance data published by Gilbert Analytics, including the Gap Benchmark, reflects past market outcomes and is not indicative of future results. Gilbert Analytics does not track or verify subscriber trading results. Actual outcomes will vary widely based on individual decisions, risk tolerance, experience, and market conditions. Investing in junior mining companies is speculative and carries a high degree of risk. You may lose some, all, or possibly more than your original investment. You are solely responsible for your own investment decisions. Always consult a licensed or registered financial professional before making any investment decision.

Alain Gilbert, B.Eng., is the founder of Gilbert Analytics.

Full disclosures at gilbertanalytics.substack.com/about